CUSTOM JAVASCRIPT / HTML

CUSTOM JAVASCRIPT / HTML

CUSTOM JAVASCRIPT / HTML

Since 2002, over 18,000 clients have turned to Dr. Stoxx for daily and weekly stock and ETF picks, options alerts, and trader training.

SIGN UP HERE

For Our FREE Weekly Pick Letter & FREE Special Report:

"How to Make Big Money Trading Breakout Stocks"

Subscribe to our Stock Pick Letters

Award-winning, consistently profitable, daily and weekly stock and ETF advisories. Now in our 16th year! Spaces are limited.

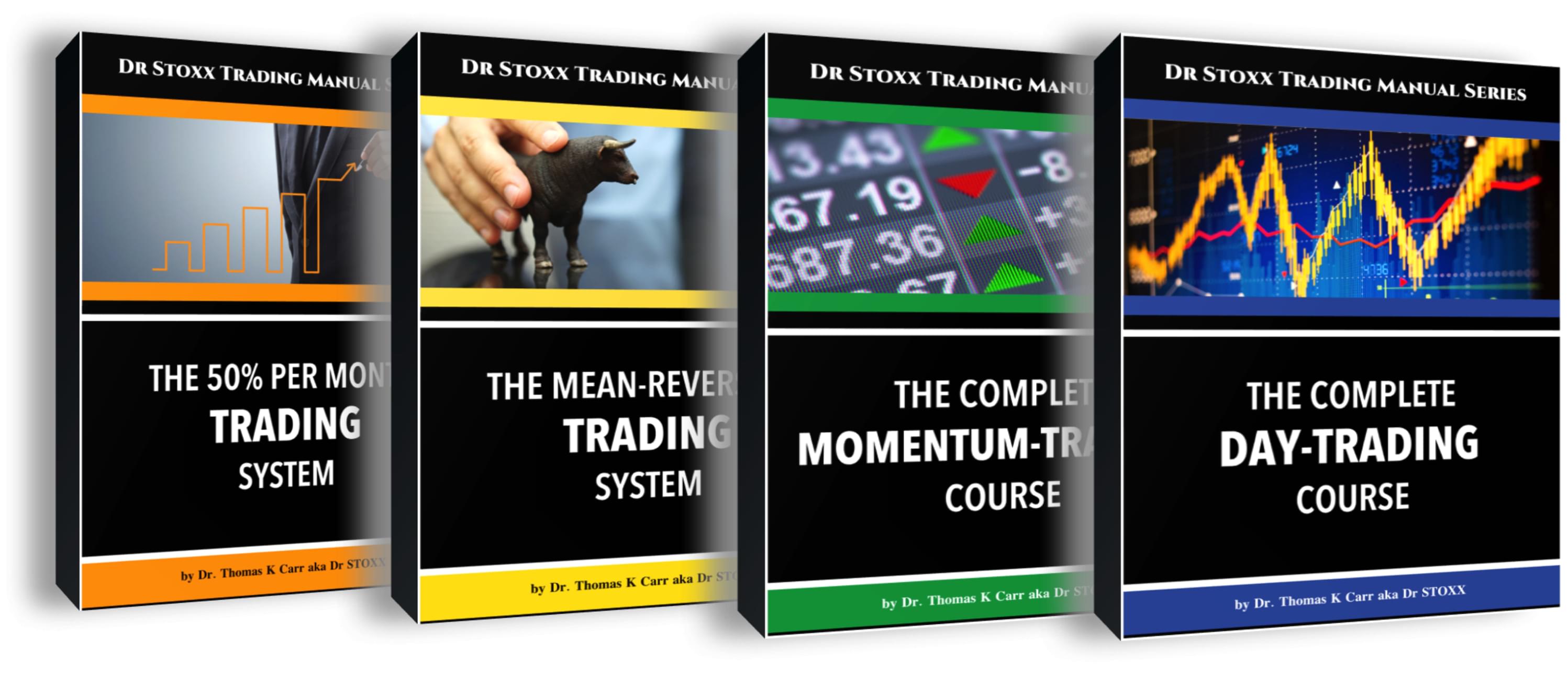

Trading Course Manuals and Webinars

Professional-grade publications and webinars give you the skills to trade for a living: Quit your day job and trade full-time!

Private Coaching and Managed Accounts

AVAILABLE NOW! Brand New Full Length Webinar!

THE DR. STOXX PULLBACK Trading System

Included: Free Month to TrendSpider ($77 value)

As featured in

Get instant access to the top picks

of one of the most successful traders in the industry.

Over 8,000 public trades, over 70% win rate, with exact entry and exit prices on every trade!

All trades posted the night before the market open! Just set it and forget it!

Dr. Stoxx serves over 18,000 clients all around the world

including hedge fund managers and financial analysts.

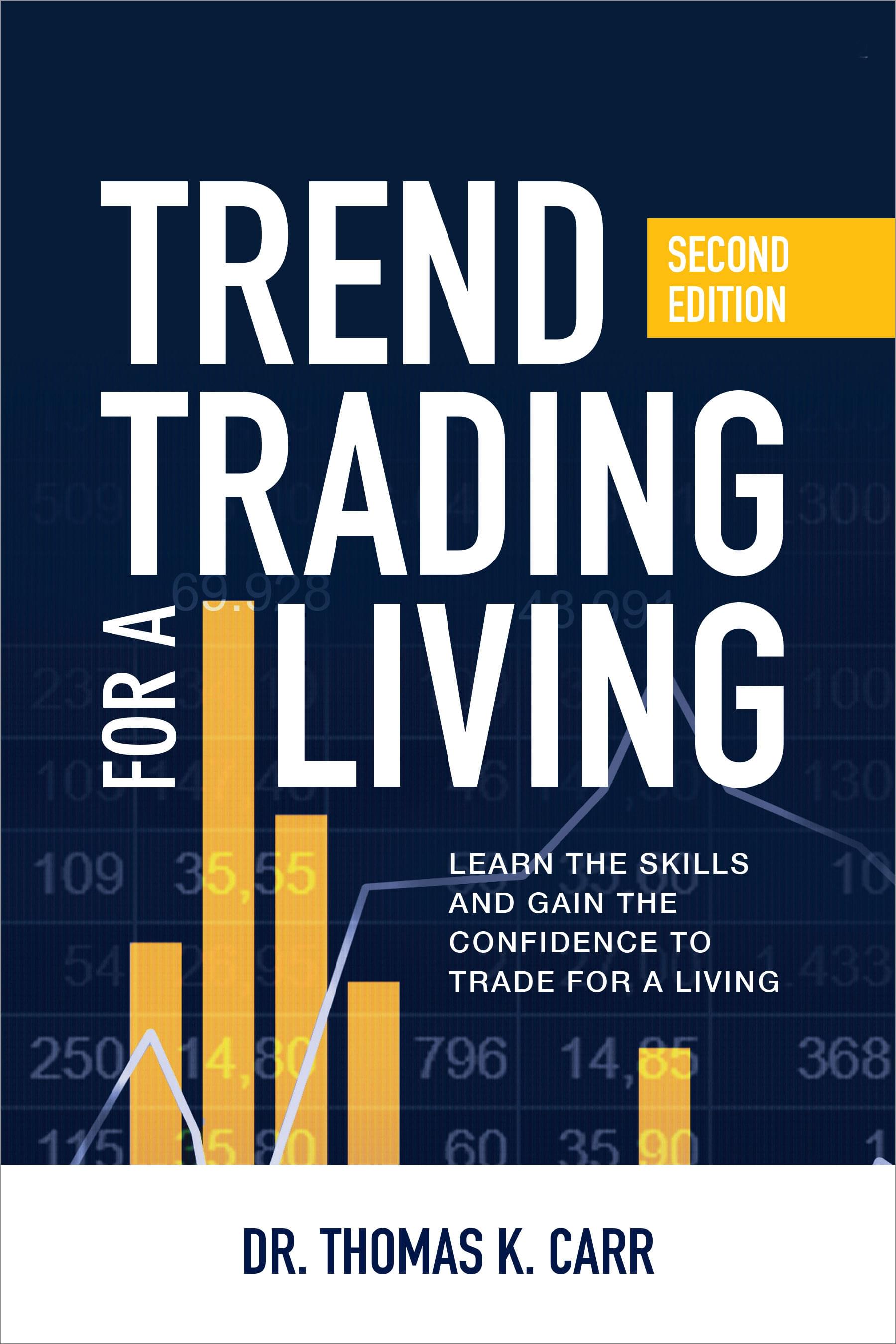

Trade with 3-Time Best Selling Author and Trading Coach

Author of the international best-seller, "Trend Trading for a Living" (McGraw Hill)

- Publisher of award-winning stock pick advisories since 2002

- Developer of over 30 market-beating trading systems

- Leading authority on momentum and smallcap tech stocks

- Trading coach with over 15,000 students, including hedge fund managers and financial analysts

- Chief Investment Strategist at Street Authority

- Best-selling author of Trend Trading for a Living

International Bestseller

Now in an All-New Updated Edition!

"Seriously nice calls this week! I'm up over $2200 in HEAR, $870 in TWLO, and another $500 in AMD. With gains from last month I paid off my credit card debt. This month we're going on a cruise! Thank you.

JP (verified subscriber), Sacramento, California

Got on board your IPO breakout in DOCU and rode it past your target for a 15-bucker. Nice! Took those winnings and bought MOMO, EVBG, and HEAR on your calls. Up huge in all three!

AM (verified subscriber), Perth, Australia

I bought CR201 course a couple of months ago. It’s absolutely wonderful! Great explanations and examples. I was of course comparing the analysis with current charts and found it right on in nearly every case. I highly recommend it. So far total net gain from your system: +$4,587 in two months.

GW (verified owner), Richmond, Virginia

Our mission is to become the #1 online site

for stock picks, market analysis, and trader training!

SIGN UP HERE

For Our FREE Weekly Pick & FREE Special Report

"How to Make Big Money Trading Breakout Stocks"

Copyright 2023 Befriend the Trend Trading, LLC. All Rights Reserved.

Disclaimer | Privacy Policy | Terms of Use | Contact

Contact: drstoxx@drstoxx.com

TERMS OF USE: Please note that stock trading is financially risky and money can be lost. All subscribers and clients agree to be responsible for any losses incurred by trading. All sales are final and there are no refunds. All subscriptions are on a recurring basis and can be cancelled at any time.

Image by Freepik

Copyright 2023 Befriend the Trend Trading, LLC. All Rights Reserved.

Disclaimer | Privacy Policy | Terms of Use | Contact

Contact: drstoxx@drstoxx.com

TERMS OF USE: Please note that stock trading is financially risky and money can be lost. All subscribers and clients agree to be responsible for any losses incurred by trading. All sales are final and there are no refunds. All subscriptions are on a recurring basis and can be cancelled at any time.

Image by Freepik